For many Irish food exporters, stepping into new markets can be as daunting as it is exciting. Most times when entering a new export market, companies will be aware they are stepping into the territory of established rivals, be they domestic players or international giants.

Since the Brexit vote in 2016, Bord Bia has developed a list of priority export markets, which will be targeted as major growth markets for Irish meat and dairy exports in the coming years. This is part of Bord Bia’s strategy to try and reduce the country’s dependence on the UK market for food exports post-Brexit.

Most of these priority markets are located in Asia, including countries such as Indonesia, Malaysia, Japan, South Korea and China.

The rapidly expanding middle classes in countries such as China, Indonesia and Vietnam, coupled with the massive food import requirement for Japan and South Korea, means there are undoubtedly opportunities in Asia for Irish food and drink.

On top of this, food and drink exports coming from Europe are seen as the pinnacle in terms of quality and consumers in these markets aspire to these products as their incomes grow.

Competition

However, from recent trade missions led by Bord Bia, it is clear that Irish exporters will face stiff competition from long-established suppliers to these markets.

For example, in countries such as Indonesia and Malaysia, Irish dairy exporters will find themselves competing directly with global dairy giants such as New Zealand’s Fonterra and Friesland Campina from the Netherlands, which both control very large market shares in each market.

Likewise, Irish meat exporters looking to do business in Japan and Korea will find themselves going head to head with US and Australian meat exporters. US exporters, in particular, have become increasingly aggressive in export markets over recent years.

Inevitably, Irish companies will need to compete on price if they are to win business, which can be difficult when going up against long-established players with real scale such as Fonterra. However, this is not to say disrupting an established player is impossible. What’s required is some different thinking and a clever strategy.

Irish companies will need to compete on price if they are to win business

One of the best examples of a new entrant cleverly disrupting long-established market leaders is the German discounter Aldi. In a little over two decades, Aldi went from zero to eking out an 8% share of the £190bn (€220bn) UK grocery market and caused massive disruption along the way.

Today, Aldi is the fifth largest retailer in the UK and continues to post double-digit sales growth, which is the envy of the established big four supermarkets (Tesco, Sainsbury’s, Asda and Morrison’s).

Disrupter

Aldi’s journey to become the great disrupter of the UK grocery market is a lesson for all Irish food exporters in strategic thinking and knowing your competitive advantage. When the German discounter first entered the UK market, it noticed one very important characteristic of the UK – it is a high-wage economy.

As such, labour is a major operating cost for big players such as Tesco and Sainsbury’s, which employ hundreds of thousands of employees between them.

In contrast, discounters such as Aldi and Lidl employ much smaller numbers of staff because their business models are built around stocking a very narrow range of products and there are no in-store bakeries, meat counters or delis that need to be manned.

As a result, labour costs for Aldi are much smaller than at established supermarkets.

The German discounter recognised very early on that its lean workforce was a major competitive advantage against the bloated operating model of the established supermarkets.

To drive this labour cost advantage home, Aldi has adopted an unusual tactic. The discounter makes a lot of noise that it pays its staff higher wages than other supermarkets.

Living wage

In Ireland, Aldi currently pays new staff at least €11.90 per hour, or the so-called “living wage”. This is considerably higher than the minimum wage rate in Ireland, which is set at €9.80 per hour since January 2019.

In the UK, Aldi pays a minimum hourly rate of £9.10, which is higher than the UK minimum wage of £8.21 per hour. For all London-based employees, the discounter pays at least £10.55 per hour. Unsurprisingly, these moves are much publicised as UK and Irish media have latched on to a feel-good story for the average worker.

As a result, established supermarkets have come under pressure to match these pay levels and wages have been driven up right across the grocery retail sector. It may seem like a counterintuitive strategy from Aldi, but a higher wage bill hurts the profit margins of the bigger supermarkets much more than it does the lean, mean German discounter.

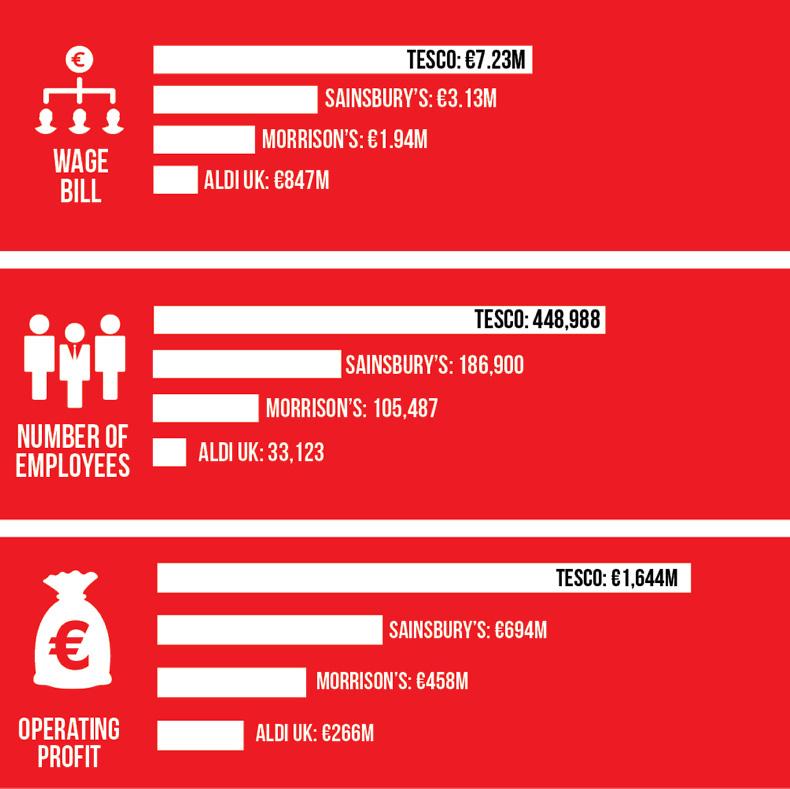

The numbers of employees working at Lidl and Aldi in the UK are dwarfed by the numbers employed by the established UK supermarkets. Combined, Tesco, Sainsbury’s and Morrisons employed close to 750,000 people in 2018 and have a combined wage bill of £12.3bn (€14.2bn).

The combined operating profits of Tesco, Sainsbury’s and Morrisons is £2.8bn (€3.2bn), meaning even a slight increase in hourly pay rates will drive up total labour costs for the established supermarkets, which will in turn eat into operating profit margins.

In contrast, Aldi employs fewer than 34,000 people in the UK and has a much smaller wage bill of £847m (€980m).

Importantly, however, Aldi’s wage bill is a smaller multiple of its operating profits, meaning it has far more room to increase pay rates than its established competitors.

An excellent illustration of the damage Aldi has inflicted on established rivals in the UK can be seen in the performance of Tesco, the UK’s largest retailer with a 27% market share today.

In 2011, Tesco was thriving. The company had annual sales in its core UK market of £45bn and operating profits of £2.5bn. Impressively, the supermarket giant boasted a profit margin above 6%. Tesco’s annual wage bill for its 492,000 odd employees stood at £6.8bn (€7.8bn), meaning it paid an average wage of just over £13,700 per annum, between part-time and full-time staff.

However, things were about to change.

With the UK in the midst of a recession like the rest of the world, squeezed UK shoppers began to switch more and more to discounters such as Aldi and Lidl to keep a lid on their weekly shopping bill.

Unwilling at first, Tesco eventually relented and began to cut prices on products to match the discounter prices. This meant eating into profit margins. However, greater challenges were still to come.

It was at this time that Aldi began to make its move to drive up labour costs against its competitors by publicising the higher wages it could offer. Tesco and others were forced to respond to these changes also.

Margins

By 2016, the landscape of UK grocery retail had changed dramatically for Tesco. Profit margins for the supermarket giant had narrowed considerably to 1.7% as operating costs spiralled and market share fell.

Despite cutting employee numbers by 10,000 from 2011 to just over 482,000 in 2016, Tesco’s wage bill actually increased by £300m in the same period to £7bn (€8.1bn). Suddenly, the supermarket found itself paying an average wage closer to £14,500 per annum.

By 2018, Tesco’s wage bill had swelled even further to £7.2bn (€8.4bn) despite reducing its employee head count by a further 33,000 people. The group’s average wage has now climbed above £16,100 per annum as a result.

At the same time, Tesco announced in its 2018 annual report that it was bringing in a 10.5% increase to hourly pay rates over a two-year period for its UK employees, which could drive Tesco’s labour costs as high as £8bn (€9.3bn).

To try and offset higher wage levels, Tesco has continued to cut employee numbers. As recently as January this year, Tesco announced it was closing the fresh food counters at up to 100 of its UK stores, which could see a further 9,000 jobs cut.

Aldi’s success in the UK market serves as an important lesson for Irish exporters seeking to compete in new markets. Established players can be disrupted with the correct strategy and knowing the competitive advantages of your business.

In just over a decade, Aldi has massively disrupted the UK grocery market and managed to inflict a lot of pain on established rivals such as Tesco, Sainsbury’s and Morrisons.

The days of fat profit margins for UK retailers look to be consigned to the past as a result of Aldi’s clever targeting of the huge numbers of employees at the established supermarkets, which has proven a major weakness.

SHARING OPTIONS